WHAT IS VALUE AVERAGING

Value Averaging is a combination of its better-known cousin

- "dollar-cost averaging" - and a process known as

"portfolio rebalancing."

The value averaging method, has been shown to produce better

results over time than the old "dollar-cost averaging"

method. Edeleson has tested VA using simulations to compare

VA to DCA and purchases of a constant number of shares in

each investment period. Without considering possible

differences in risk, Edleson concludes:

-

“There is

an inherent return advantage of value averaging (over

dollar-cost averaging and purchase of a constant number

of shares).”

-

“It’s about

as close to ‘buy low, sell high’ as we’re going to get

without a crystal ball.”

Edleson, who was also a managing director at Morgan Stanley

(MS), relied on one crucial piece of information that was

missing from the "dollar-cost averaging" method to come up

with "value averaging." By considering a portfolio’s

expected rate of return (something that the "dollar-cost

averaging" method neglects), the value averaging method

helps to identify periods of over and underperformance.

When a portfolio is underperforming, share prices are likely

to be low. And that’s when you’ll be investing more to make

up for the underperformance. When the portfolio is

outperforming your target rate return, share prices are

likely to be high. That means it is not a good time to buy

and you could even sell for a profit, provided you maintain

your predetermined average growth rate.

Value Averaging is a nice way to ensure you follow one of

the most well known investment mandates: Buy low and sell

high. The method is particularly valuable during

times of high volatility to help ensure investors

maintain discipline in their investing. And in these

difficult market conditions, it’s certainly worth

considering.

“The rule under value averaging is simple: ... make the

value not (the market price) of your investment go up by a

fixed amount each month.”

HOW VALUE

AVERAGING WORKS

Basically, the idea behind

dollar-cost averaging is that instead of investing a sum of

money all at once, you invest it a little bit at a time over

a specific period. So, for example, if at the beginning of

the year you had $12,000 that you wanted to invest in

stocks, you might invest $1,000 each month over the course

of a year instead of investing it all at once. This is

essentially Dollar Cost Averaging where the idea is that you

reduce risk because you're buying stocks at a variety of

prices throughout the year instead of buying all the shares

at a single price. Dollar cost averaging is a “Buy low, buy

less high” strategy, as there are no rules for selling.

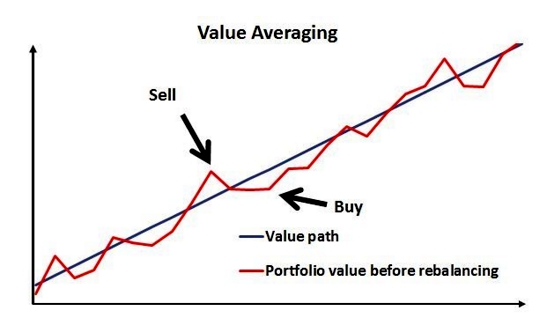

Value Averaging works a bit

differently. With Value Averaging, you first figure out how

much money you will need to accumulate for a goal such as

retirement. Then, based on the annualized return you expect

to earn on your investments, you figure out how much you

must invest each month to achieve that goal.

So let's say you have a goal of

accumulating $500,000 over the next 20 years. If you figure

you can earn an annualized 8 percent, then you would need to

put away about $875 a month. You can then chart your

progress month by month towards that goal. Here's where the

"value" part of value averaging comes in. Let's say that, at

the end of the first year, instead of having the $10,950 you

should have to be on track toward your goal, a downturn in

the markets leaves you with just $10,000.

That would mean that the next

month, instead of investing your usual $875, you would

invest an additional $950 to bring your portfolio's value to

where it should have been to remain on track toward your

goal. In fact, you would go through this process each month.

In months where you fall behind, you would add to the amount

you invest each month. And in months where your returns are

higher than expected and your portfolio's value gets beyond

where it needs to be, you would scale back your monthly

investment, or even possibly end up selling some shares. Hence, value averaging provides sell signals so when properly applied, it should help us to "buy low, sell high".

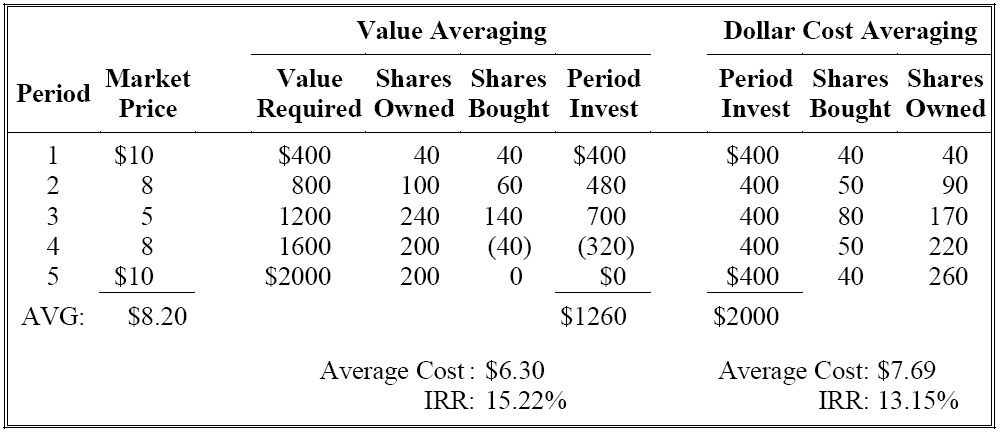

HOW VALUE AVERAGING DIFFERS AND WHY IT

WORKS

While either approach (VA or DCA) could dominate over any time

period, value averaging has the edge most of the time because it is more

aggressive. However, value averaging requires more monitoring,

has more transaction costs, and because it triggers sales,

potentially more tax consequences. Value averaging can be

modified so that no sales take place, with future value

increases adjusted to compensate. Also, the loss potential is

greater for value averaging because the total amount that is

required to be invested is unconstrained.

At

first glance the VA strategy may not seem too different from DCA,

however there are significant differences:

-

A large upward

price swing often results in the sale of shares, instead of

a purchase.

-

VA also results

in a net average cost per share that is much lower than the

average cost per share with DCA.

-

There is often

a tendency to sell shares when the share price is high; the

best DCA can do is buy fewer of the more expensive shares

-

VA takes a more

extreme response to market dips and rises than does DCA. The

return is enhanced greatly by the larger purchases at low

prices and by the profit taking as shares are sold at

generally higher prices.

-

VA forces you

to avoid big moves into a peaked market or panic selling at

the bottom

-

VA tends to

provide the highest returns in the stock market over short

to immediate term investment periods.

Value Averaging (like DCA) helps investors to

tide over market volatility without worrying too much about

market timing.

|